Directors and Officers Liability Policy Insurance

Protects leaders from legal claims arising from their decisions and actions.

Protect Personal Assets

Safeguard your personal wealth against legal claims.

Manage Legal Risks

Cover the costs of defending against lawsuits and claims.

Attract Top Talent

Offer security and confidence to potential directors and officers.

Ensure Corporate Governance

Support sound decision-making and protect against managerial errors.

Protect Personal Assets

Safeguard your personal wealth against legal claims.

Manage Legal Risks

Cover the costs of defending against lawsuits and claims.

Attract Top Talent

Offer security and confidence to potential directors and officers.

Ensure Corporate Governance

Support sound decision-making and protect against managerial errors.

Leadership Protection

Protects directors and officers from personal financial liability.

Legal Defense Coverage

Covers legal costs, settlements, and judgments from claims.

Liability Protection

Covers claims from shareholders, regulators, or stakeholders.

Executive Confidence

Allows leaders to make decisions without fear of personal risk.

Who’s this for?

Who’s this for?

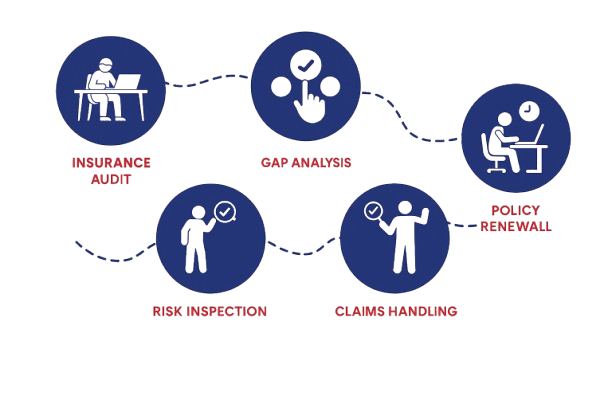

Submission

Assessment