Workmen Compensation

Protect all your employees from medical emergencies

Protect Your Workforce

Comprehensive protection for your employees against workplace risks.

Compliance Made Easy

Ensure legal and financial safety with a robust compensation plan.

Emergency Support Assurance

Be prepared to meet medical and financial obligations effectively.

Safety and Security First

Strengthen your employer-employee bond with reliable compensation.

Comprehensive Protection for Your Workforce

Ensure employee well-being with complete health insurance coverage.

Cost-Effective Group Insurance Plans

Affordable plans with benefits like maternity, critical illness, and dependent coverage.

Peace of Mind for Employers and Employees

Reduce financial stress with cashless claims and reimbursement options.

Boost Employee Productivity and Retention

Build loyalty and motivation by easing economic and mental burdens.

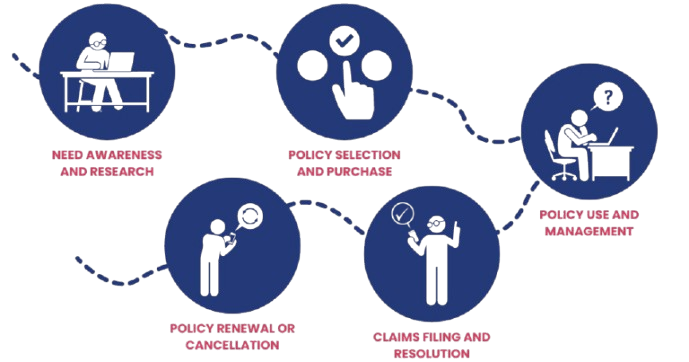

Who’s this for?

Who’s this for?

Sub-contractor Cover

If a contractor hires a sub-contractor without WC coverage, the contractor can add this specific coverage to ensure the sub-contractor's employees are covered under WC.

Medical Extension

This add-on extends medical coverage for workers who are hospitalized for more than 24 hours due to an injury or illness incurred at work.

Terrorism

A specialized add-on covering losses caused by terrorist attacks, extending the WC coverage beyond conventional accidents.

Occupational Disease

Covers illnesses caused by the workplace environment, including conditions like Compressed Air Disease from high or low-pressure areas such as tunnels or underwater sites.

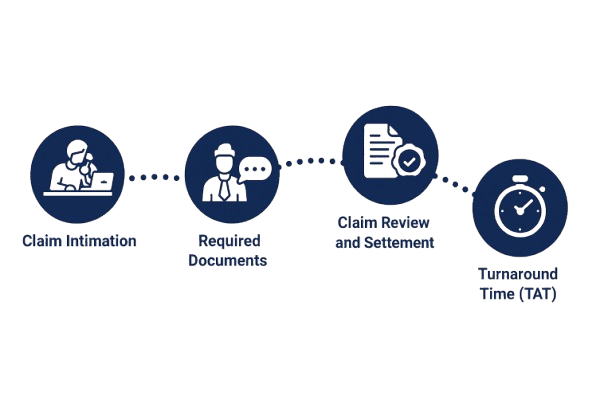

Submission

Assessment